Popular information

Popular science background:

The quest for the perfect auction (pdf)

Populärvetenskaplig information:

Jakten på den perfekta auktionen (pdf)

![]()

The Prize in Economic Sciences 2020

Every day, auctions distribute astronomical values between buyers and sellers. This year’s Laureates, Paul Milgrom and Robert Wilson, have improved auction theory and invented new auction formats, benefitting sellers, buyers and taxpayers around the world.

The quest for the perfect auction

Auctions have a long history. In Ancient Rome, lenders used auctions to sell the assets they had confiscated from borrowers who were unable to pay their debts. The world’s oldest auction house, Stockholms Auktionsverk, was founded in 1674 – also for the purpose of selling appropriated property.

Nowadays, when we hear the word auction, we perhaps think of traditional farm auctions or high-end art auctions – but it could just as well be about selling something on the internet or buying property via an estate agent. Auction outcomes are also very important for us as taxpayers and as citizens. Often, the companies that manage our home refuse collection have won a public procurement by placing the lowest bid. Flexible electricity prices, which are determined daily in regional electricity auctions, influence the cost of heating our homes. Our mobile phone coverage depends on which radio frequencies the telecom operators have acquired through spectrum auctions. All countries now take loans by selling government bonds in auctions. The purpose of the European Union’s auction of emission allowances is to mitigate global warming.

So, auctions affect all of us at every level. Moreover, they are becoming increasingly common and increasingly complicated. This is where this year’s Laureates have made major contributions. They have not just clarified how auctions work and why bidders behave in a certain way, but used their theoretical discoveries to invent entirely new auction formats for the sale of goods and services. These new auctions have spread widely around the world.

Auctions are everywhere and affect our everyday lives – they decide the prices of electricity, emission allowances, financial assets and various commodities.

Auction theory

To understand the Laureates’ contributions, we need to know a little more about auction theory. The outcome of an auction (or procurement) depends on three factors. The first is the auction’s rules, or format. Are the bids open or closed? How many times can participants bid in the auction? What price does the winner pay – their own bid or the second-highest bid? The second factor relates to the auctioned object. Does it have a different value for each bidder, or do they value the object in the same way? The third factor concerns uncertainty. What information do different bidders have about the object’s value?

Using auction theory, it is possible to explain how these three factors govern the bidders’ strategic behaviour and thus the auction’s outcome. The theory can also show how to design an auction to create as much value as possible. Both tasks are particularly difficult when multiple related objects are auctioned off at the same time. This year’s Laureates in Economic Sciences have made auction theory more applicable in practice through the creation of new, bespoke auction formats.

Different types of auctions

Auction houses around the world usually sell individual objects using an English auction. Here, the auctioneer begins with a low price, and subsequently suggests increasingly higher prices. The participants can see all the bids and choose whether they want to place a higher one. Whoever has placed the highest bid wins the auction and pays what she bid. But other auctions have completely different rules; a Dutch auction starts with a high price, which is then gradually lowered until the object is sold.

Both the English and Dutch auctions have open bids, so all participants see the others’ bids. In other types of auctions, however, the bids are closed. In public procurements, for example, the bidders often place sealed bids and the procurer chooses the supplier that commits to performing the service at the lowest price, provided that specific quality requirements are fulfilled. In some auctions, the final price is the highest bid (first-price auctions), but in other formats the winner pays the second-highest bid (second-price auctions).

Which auction format is best? This not only depends on the outcome, but also on what we mean by “best”. Private sellers are usually most concerned with getting the highest price. Public sellers have broader aims, such as the goods being sold to the bidder that delivers the most long-term benefit for society as a whole. The quest for the best auction is a tricky problem that has occupied economists for a long time.

The difficulty with auction analysis is that a bidder’s best strategy depends on how she believes the other participants will bid in the auction. Do some bidders believe the object is worth more or less than others? Do these different valuations reflect some bidders having better information about the goods’ characteristics and value? Can bidders cooperate and manipulate the auction to keep the final price down?

Private values

The 1996 Laureate in Economic Sciences, William Vickrey, established auction theory in the early 1960s. He analysed a special case, in which the bidders only have private values for the good or service being auctioned off. This means that the bidders’ values are entirely independent of each other. For instance, this could be a charity auction for dinner with a celebrity (say a Nobel Laureate). How much you are willing to pay for such a dinner is subjective – your own valuation is not affected by how other bidders value the dinner. So how should you bid in this type of auction? You should not bid more than the dinner is worth to you. But should you bid lower, perhaps getting the dinner at a lower price?

Vickrey showed that the best-known auction formats – such as the English and the Dutch – give the same expected revenue to the seller, provided that all bidders are rational and risk neutral.

Common values

Entirely private values are an extreme case. Most auction objects – such as securities, property and extraction rights – have a considerable common value, meaning that part of the value is equal to all potential bidders. In practice, bidders also have different amounts of private information about the object’s properties.

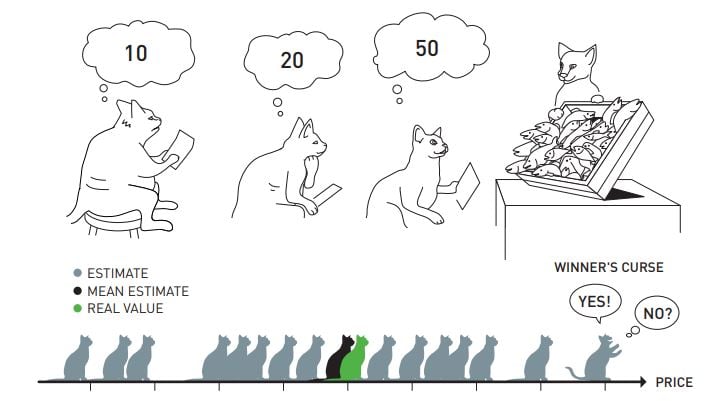

Let’s take a concrete example. Imagine that you are a diamond dealer and that you – as well as some other dealers – are contemplating a bid on a raw diamond, so you can produce cut diamonds and sell them on. Your willingness to pay only depends on the resale value of the cut diamonds which, in turn, depends on their number and quality. Different dealers have different opinions about this common value, depending on their expertise, experience and the time they have had to examine the diamond. You could assess the value better if you had access to the estimates of all the other bidders, but each bidder prefers to keep their information secret.

Bidders in auctions with common values run the risk of other participants having better information about the true value. This leads to the well-known phenomenon of low bids in real auctions, which goes by the name of the winner’s curse. Say that you win the auction of the raw diamond. This means that the other bidders value the diamond less than you do, so that you may very well make a loss on the transaction.

The most optimistic bidder often overestimates the common value of an auctioned object, so that ‘winning’ the auction turns out to cause a loss – the winner’s curse.

Robert Wilson was the first to create a framework for the analysis of auctions with common values, and to describe how bidders behave in such circumstances. In three classic papers from the 1960s and 1970s, he described the optimal bidding strategy for a first-price auction when the true value is uncertain. Participants will bid lower than their best estimate of the value, to avoid making a bad deal and thus be afflicted by the winner’s curse. His analysis also shows that with greater uncertainty, bidders will be more cautious and the final price will be lower. Finally, Wilson shows that the problems caused by the winner’s curse are even greater when some bidders have better information than others. Those who are at an information disadvantage will then bid even lower or completely abstain from participating in the auction.

Both private and common values

In most auctions, the bidders have both private and common values. Suppose you are thinking about bidding in an auction for an apartment or a house; your willingness to pay then depends on your private value (how much you appreciate its condition, floor plan and location) and your estimate of the common value (how much you might be able to sell it for in the future). An energy company that bids on the right to extract natural gas is concerned with both the size of the gas reservoir (a common value) and the cost of extracting the gas (a private value, as the cost depends on the technology available to the company). A bank that bids for government bonds considers the future market interest rate (a common value) and the number of their customers who want to buy bonds (a private value). Analysing bids in auctions with private and common values turned out to be an even trickier problem than the special cases analysed by Vickrey and Wilson. The person who finally cracked this nut was Paul Milgrom, in a handful of papers published around 1980.

Milgrom’s analysis – partly with Robert Weber – included new and important insights about auctions. One of these concerns how well different auction formats deal with the problem of the winner’s curse. In an English auction, the auctioneer starts with a low price and raises it. Bidders who observe the price at which other bidders drop out of the auction therefore obtain information about their valuations; as the remaining bidders then have more information than at the start of the auction, they are less prone to bid below their estimated value. On the other hand, a Dutch auction, where the auctioneer starts with a high price and reduces it until someone is willing to buy the object, does not generate any new information. The problem with the winner’s curse is thus greater in Dutch auctions than in English auctions, which results in lower final prices.

This particular result reflects a general principle: an auction format provides higher revenue the stronger the link between the bids and the bidders’ private information. Therefore, the seller has an interest in providing participants with as much information as possible about the object’s value before the bidding starts. For example, the seller of a house can expect a higher final price if the bidders have access to an (independent) expert valuation before bidding starts.

Better auctions in practice

Milgrom and Wilson have not only devoted themselves to fundamental auction theory. They have also invented new and better auction formats for complex situations in which existing auction formats cannot be used. Their best-known contribution is the auction they designed the first time the US authorities sold radio frequencies to telecom operators.

Radio frequencies that permit wireless communication – mobile phone calls, internet payments, or video meetings – are limited resources of great value to consumers, businesses and society. These frequencies are government owned, but private actors can often utilise them more efficiently. The authorities thus had to somehow allocate access to frequency bands to these actors. This was initially done through a process known as a beauty contest, in which companies had to provide arguments for why they, in particular, should receive a licence. This process meant that telecom and media companies spent huge amounts of money on lobbying. The revenue generated by the process was limited, however.

In the 1990s, as the market for mobile telephony expanded, the responsible authority in the US, the Federal Communications Commission (FCC), realised that beauty contests were no longer tenable. The number of mobile companies had expanded rapidly, and the FCC was practically drowning in applications for access to the radio frequencies. After pressure from the FCC, the US Congress permitted the use of lotteries for allocating frequency bands. The beauty contest was thus replaced by an entirely random allocation of licences, which likewise generated only limited income for the government.

However, the mobile operators were unhappy. The lotteries were held at local level, so national mobile operators would typically get entirely discontinuous networks with different frequency bands in different regions. The operators then tried buying and selling frequencies between themselves, leading to the emergence of a large second-hand market for licences. Meanwhile, the US’ growing national debt made it increasingly politically difficult to continue distributing licences almost for free. The market value of the licences was many billions of dollars – money that ended up in the hands of frequency speculators instead of in the US Treasury (a loss of revenue which would ultimately be borne by taxpayers). Finally, in 1993, it was decided that frequency bands would be distributed using auctions.

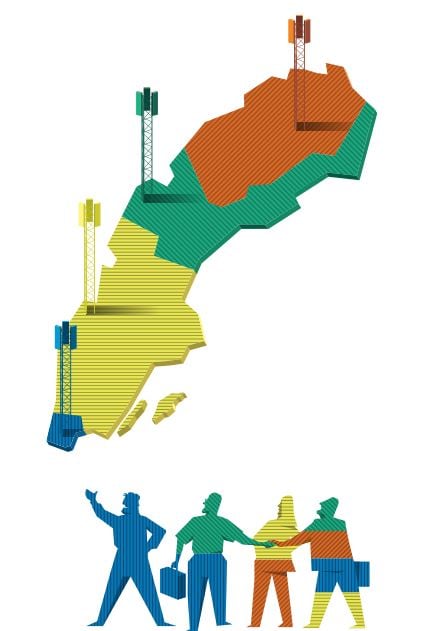

Participants in auctions of multiple interrelated objects – such as radio frequencies in different parts of the country – often want to bid on “packages” of objects. This complicates the auction’s design, especially if the seller wants to stop bidders from colluding to keep prices low.

New auction formats

Now a new problem arose – how do you design an auction that achieves the efficient allocation of radio-frequency bands, while at the same time benefitting taxpayers to the greatest possible extent? This problem turned out to be very difficult to solve, since a frequency band has both private- and common-value components. Also, the value of a specific frequency band in a specific region depends on the other frequency bands owned by a specific operator.

Consider an operator who wants to build a national mobile network. Say that a Swedish regulator auctions off frequency bands one by one, starting with Lapland in the north, and onward across the country down to Skåne in the south. Now the value of the Lapland licence depends on whether the operator – in later rounds – succeeds in buying licences all the way down to Skåne, and at what price. The operator does not know the outcomes of future auctions, so it is almost impossible to know how much they should pay for the licence. In addition, speculative buyers may try to purchase the exact frequency band the operator needs in Skåne, so they can sell it at a high price on the second-hand market. Because there is great uncertainty, the operator will keep its bid low or entirely withdraw from the auction to await a possible second-hand market.

This stylised Swedish example illustrates a general problem. To circumvent it, the first US auction had to allocate all the geographic areas of the radio spectrum in one go. It also had to manage many bidders. To tackle these problems, Milgrom and Wilson – partly with Preston McAfee – invented an entirely new auction format, the Simultaneous Multiple Round Auction (SMRA). This auction offers all objects (radio frequency bands in different geographic areas) simultaneously. By starting with low prices and allowing repeated bids, the auction reduces the problems caused by uncertainty and the winner’s curse. When the FCC first used an SMRA in July 1994, it sold 10 licences in 47 bidding rounds for a total of 617 million dollars – objects which the American government had previously allocated practically for free.

The first spectrum auction using an SMRA was generally regarded as a huge success. Many countries (including Finland, India, Canada, Norway, Poland, Spain, the UK, Sweden, and Germany) adopted the same format for their spectrum auctions. The FCC’s auctions alone, using this format, have brought more than 120 billion dollars over twenty years (1994–2014) and, globally, this mechanism has generated more than 200 billion dollars from spectrum sales. The SMRA format has also been used in other contexts, such as sales of electricity and natural gas.

Subsequently, auction theorists – often working with computer scientists, mathematicians and behavioural scientists – have refined the new auction formats. They have also adapted them to reduce the opportunities for manipulation and cooperation between bidders. Milgrom is one of the architects of a modified auction (the Combinatorial Clock Auction) in which operators can bid on “packages” of frequencies, rather than individual licences. This type of auction requires significant computational capacity, as the number of possible packages grows very quickly with the number of frequencies for sale. Milgrom is also a leading developer of a novel format with two rounds (the Incentive Auction). In the first round, you buy radio spectra from current licence-holders. In the second round, you sell these relinquished frequencies to other actors who can manage them more efficiently.

Basic research led to new inventions

Milgrom and Wilson’s ground-breaking initial work should be regarded as basic research. They wanted to use and develop game theory to analyse how different actors behave strategically when they each have access to different information. Auctions – with their clear rules that govern this strategic behaviour – comprised a natural arena for their research. However, auctions have gained in practical significance and, since the mid-1990s, they have been increasingly used in the distribution of complex public assets, such as frequency bands, electricity and natural resources. Fundamental insights from auction theory provided the foundation for constructing new auction formats that overcame these new challenges.

The new auction formats are a beautiful example of how basic research can subsequently generate inventions that benefit society. The unusual feature of this example is that the same people developed the theory and the practical applications. The Laureates’ ground-breaking research about auctions has thus been of great benefit, for buyers, sellers and society as a whole.

Further reading

Additional information on this year’s prizes, including a scientific background in English, is available on the website of the Royal Swedish Academy of Sciences, www.kva.se, and at www.nobelprize.org, where you can watch video footage of the press conferences, the Nobel Lectures and more. Information on exhibitions and activities related to the Nobel Prizes and the Prize in Economic Sciences is available at www.nobelprizemuseum.se

The Royal Swedish Academy of Sciences has decided to to award the Sveriges

Riksbanks Prize in Economic Sciences in Memory of Alfred Nobel 2020 to

PAUL R. MILGROM

Born 1948 in Detroit, USA.

Ph.D. 1979 from Stanford University,

Stanford, USA. Shirley and Leonard

Ely, Jr. Professor of Humanities and

Sciences, Stanford University,

Stanford, USA.

ROBERT B. WILSON

Born 1937 in Geneva, USA.

D.B.A.1963 from Harvard University,

Cambridge, USA. Adams Distinguished

Professor of Management, Emeritus,

Stanford University, Stanford, USA

“for improvements to auction theory and inventions of new auction formats”

Science Editors: Tommy Andersson, Tore Ellingsen, and Torsten Persson, Committee for the Prize in Economic Sciences in Memory of Alfred Nobel

Translator: Clare Barnes

Illustrations: © Johan Jarnestad/The Royal Swedish Academy of Sciences

Editor: Eva Nevelius

© The Royal Swedish Academy of Sciences

Nobel Prizes and laureates

Six prizes were awarded for achievements that have conferred the greatest benefit to humankind. The 12 laureates' work and discoveries range from proteins' structures and machine learning to fighting for a world free of nuclear weapons.

See them all presented here.